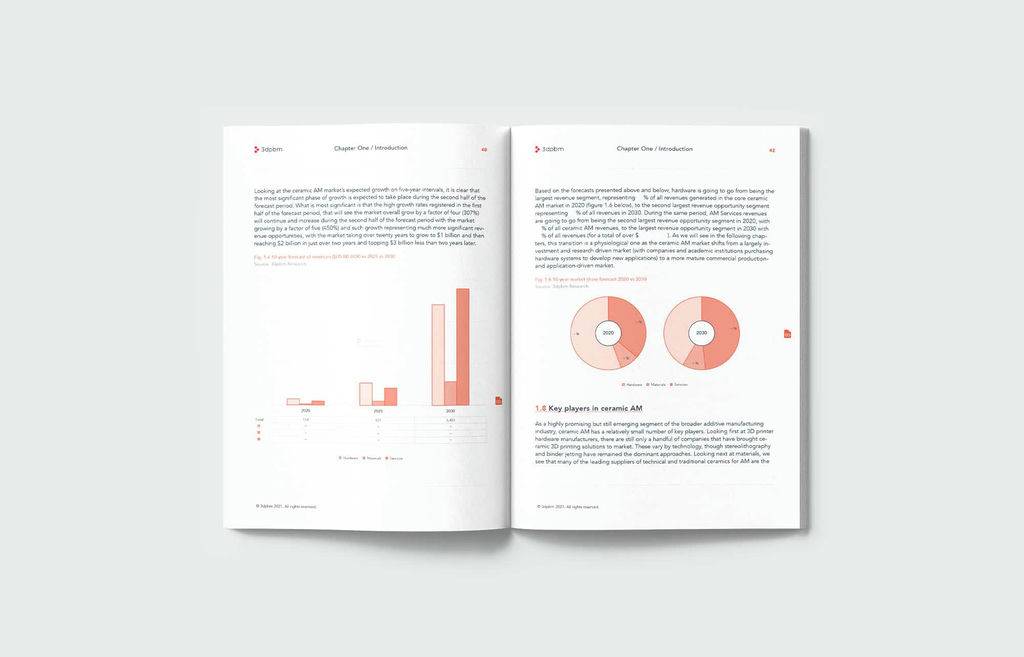

In the recent 3dpbm Report on Ceramic Additive Manufacturing we looked with unprecedented depth at the ceramic AM market finding that the opportunities are there and must be pursued. Here’s how.

The overall ceramic manufacturing market, including both technical ceramics such as alumina and zirconia, and sand materials is currently worth as much as $400 billion yearly. According to the latest study we conducted at 3dpbm Research, ceramic additive manufacturing today is worth less than 0.05% of that. That’s a lower penetration than metal AM and polymer AM in their respective addressable markets. Why is that? The level of technology readiness is part of it but mostly it is because of lack of awareness.

Ceramics are both some of the oldest used materials and the most advanced materials for humanity’s future. As such, many of the companies that use ceramic in their manufacturing do so with consolidated, traditional processes and they are generally not very open to change. But to better understand where the opportunities lie in the ceramic additive manufacturing we need to separate between traditional and technical ceramics.

That is what we did in 3dpbm’s Ceramic Additive Manufacturing Opportunities and Trends report, where we identified 96 companies (about 50% split between traditional and technical ceramic companies), including AM hardware manufacturers, AM materials suppliers and AM service providers. In total, the dataset for this market study comprises over 6,000 data points, providing one of the most accurate snapshots of the current ceramic AM global market.

The market leaders in technical ceramics today are hardware companies such as Lithoz, ExOne and 3DCeram. Lithoz and 3DCeram develop systems for stereolithography 3D printing of advanced technical ceramics which mainly include alumina, zirconia, silicon nitride and some calcium-based ceramics such as TCP and HA (hydroxyapatitie) for medical and implants applications. The primary revenue opportunity in technical ceramic today is in hardware because the ceramic industry still needs to develop enough application cases to enable more production initiatives.

Some of the most advanced ceramic companies are now investing in ramping up both their ceramic AM prototyping and production capabilities. More companies will follow because AM enables production of ceramic part geometries and subassemblies that cannot be made in any other way, especially not with digital subtractive methods since many of these ceramics are very difficult and costly to cut. Complex ceramic 3D printed parts are needed in the aerospace, energy, dental/medical and consumer products/jewelry segments. Silicate ceramic are also used to produce intricate foundry cores, for production of metal parts in the energy and aerospace segment. Other opportunities are now emerging in production of large silicon carbide parts using direct binder jetting technology.

In traditional ceramics the scenario is radically different. Here the primary benefits are clearly visibile especially in the foundry industry, for rapid production of complex casts and cores. The biggest hurdle here is the initial CapEx investment required as these technologies, provided primarily by ExOne and Voxeljet, require very large, expensive machines. However, awareness is the ultimate hurdle, since the value proposition of implementing additive for foundry cast and core production has been clearly established based on several real application cases presented in our report. Although the rate of adoption is slow, more and more foundries and sand 3D printing services providers, especially in the US and in Germany, are now starting to adopt and offer these capabilities. In fact, GE recently announced a collaboration with voxeljet to build the largest sand binder jetting machine in the world to make casts for giant single parts of the Halyade-X wind turbines.

Ultimately, I have no doubt that ceramics are key materials for the future of humanity. Engineers will need to increasingly turn to ceramics when they have exhausted the possibilities of metals and advanced polymers, using AM to push part geometry. At the same time, more and more companies will be able to transition to 3D printing of sand casts and cores, without having to depart from their current use of casting processes, while benefiting from AM to produce more complex parts.